If you’ve been digging into IPOs, you’ve probably noticed QIBs and anchor investors mentioned together, but they’re not the same thing.

Both are big institutional players, yet they play different roles in the allocation game.

Here’s the straightforward breakdown of difference between QIBs and anchor investors in IPO, focusing on timing, quotas, and how this fits into the overall IPO cycle stages and process.

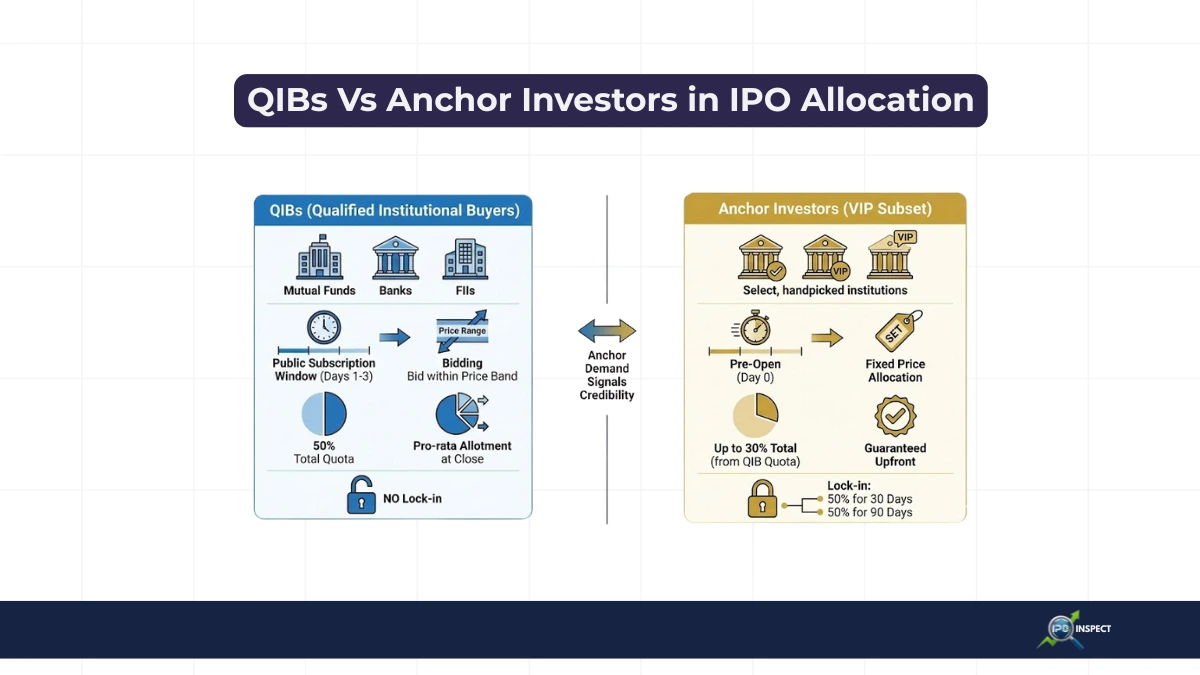

What is QIB and Anchor Investors in IPO

QIBs (Qualified Institutional Buyers) are the broad category of heavyweights like mutual funds, FIIs, banks, and insurance companies who qualify for the massive 50% IPO quota under SEBI’s QIB definition in IPOs. They’re the smart money that bids during the public subscription window.

Anchor Investors are a special subset within QIBs select institutions handpicked to commit big money a day before the IPO opens to everyone else. Their job? Kick things off with credibility.

Key Differences Between QIBs and Anchor Investors in IPO Allocation

Here’s where they diverge most clearly especially around how shares land (or don’t) in demat accounts:

| Aspect | QIBs (Regular) | Anchor Investors |

|---|---|---|

| Timing | Bid during 3-5 day public window | Allocated 1 day before public open |

| Quota Source | Full 50% of net issue | Up to 60% of QIB quota (max 30% total issue), typically disclosed in the DRHP for the IPO |

| Minimum Bid | No strict minimum (but institutional scale) | ₹10 Cr (mainboard); ₹2 Cr (SME) |

| Allotment Style | Pro-rata or discretionary during close | Guaranteed upfront at fixed price |

| Lock-in Period | None | 50% for 90 days; 50% for 30 days |

| Price Discovery | Bid within band; influence final price | Fixed price (often slight discount); disclosed pre-open |

| Withdrawal | Limited after half the window | No withdrawal allowed |

| Disclosure | Post-subscription in live data | Names & amounts public pre-IPO |

Anchors get VIP treatment to build hype, strong names like HDFC MF or SBI signal this IPO is solid and often support expectations of high listing gains in IPOs.

How Allocation Plays Out Differently

For QIBs: Shares spread across the pool via pro-rata (everyone gets a slice proportional to bids) once subscription ends. Heavy oversubscription? Even big funds might get scaled back. No special lock-in means they can sell on listing day if they want.

For Anchors: Allocation happens upfront, often cherry-picked by the company. It’s discretionary, merchant bankers favor reputable players. That lock-in (30/90 days split) prevents immediate dumping, stabilizing early trading. Their commitment fills ~1/3 of QIB quota right away.

Example: ₹1000 Cr IPO reserves ₹500 Cr for QIBs. Anchors might snag ₹300 Cr day zero (disclosed publicly), leaving ₹200 Cr for other QIBs to fight over during the window.

Why This Split Matters to Retail Investors Like You

- Signal strength: Heavy anchor participation (especially quality names) often predicts good listing gains as it shows conviction investors can later verify this by tracking past IPO listing gains.

- Subscription boost: Anchors “anchor” demand, encouraging NIIs and retail to pile in.

- Price stability: Lock-in reduces Day 1 volatility from big sellers.

Weak anchors? Tread carefully, might mean lukewarm institutional interest.

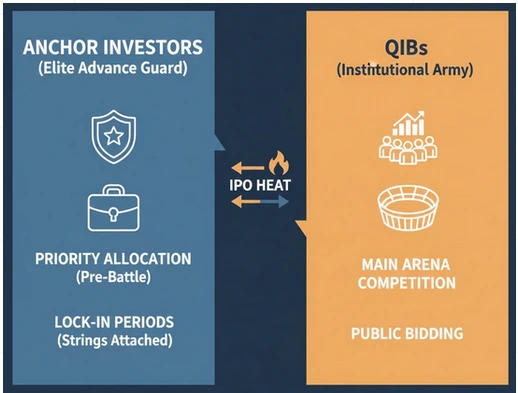

Real-World Takeaway:

QIBs are the entire institutional army bidding publicly, anchors are the elite advance guard locking in pre-battle. In allocation terms, anchors get priority slices with strings attached, while regular QIBs compete in the main arena.

Track both in RHPs and live data to gauge IPO heat, alongside indicators like IPO GMP today that reflect real-time market sentiment.