If you’ve scanned a few IPO prospect uses, QIB probably jumped out at you right alongside retail and NII category in IPO.

It’s one of those acronyms that sounds intimidating but really just points to the big players who anchor most public issues.

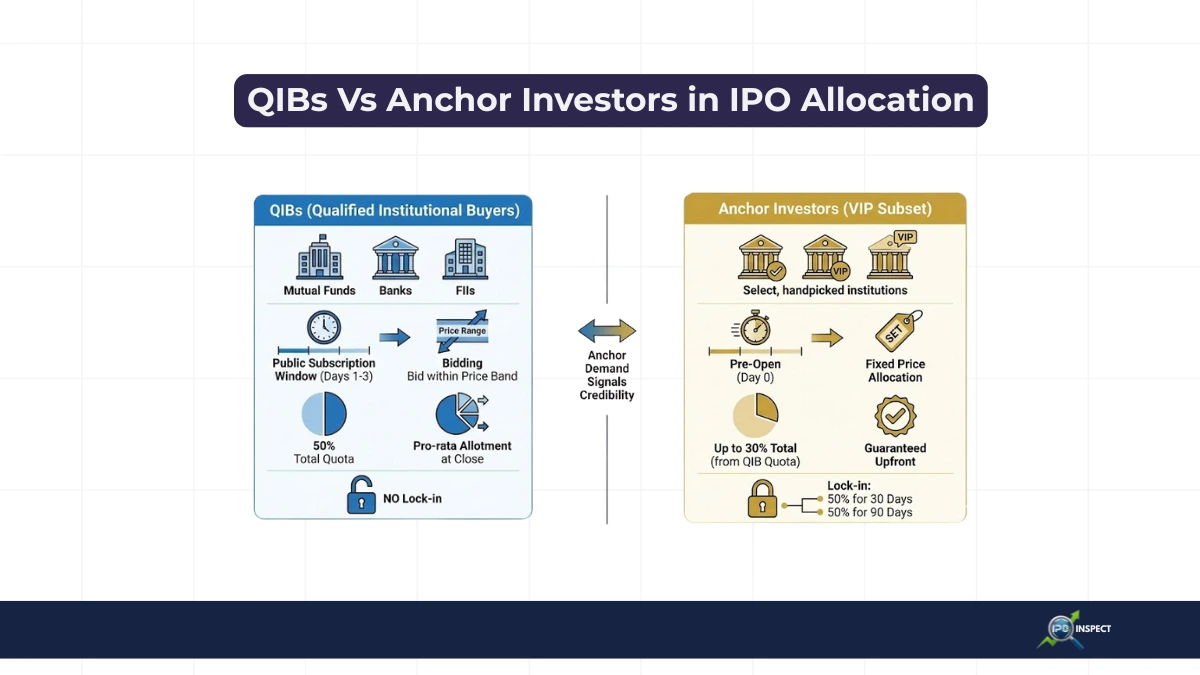

QIB stands for Qualified Institutional Buyer, and they’re the heavyweights think mutual funds and FIIs who get first dibs on about half the shares. Let me unpack it without the jargon overload.

Who Qualifies as QIB in an IPO?

QIBs aren’t your average Joes, they’re SEBI registered institutions with deep pockets and market smarts. Here’s the usual lineup:

- Mutual funds and insurance companies managing billions for highest listing gain IPO in india.

- Foreign Portfolio Investors (FPIs) and foreign venture capital funds.

- Banks, pension funds, and public financial institutions.

- Even multilateral agencies like IFC or ADB if they’re in the mix.

These institutions study the DRHP IPO in detail and rely on deep IPO analysis and evaluation before committing large bids.

The key, They handle massive assets (often ₹100+ crore portfolios) and have the chops to dig into company filings without hand-holding.

QIB Quota: Their Slice of the IPO Pie

SEBI carves out roughly 50% of the net issue for QIBs in book-built and IPO price band details, sometimes up to 60% if the company skips profitability tests. This isn’t random, it’s deliberate to draw smart money that signals quality to everyone else.

| Category | Typical Quota | Who They Are |

|---|---|---|

| QIB | 50% | Institutions like MFs, FIIs |

| Retail | 35% | Individuals applying upto ₹2 lakh with maximum lot size in IPO |

| NII | 15% | HNIs over ₹2L |

Anchor investors (a QIB subset) lock in 30–60% of this quota a day before opening, often at a slight discount that influences how is IPO listing price decided.

How QIBs Shape the IPO Game

These guys bid big in the IPO book, helping set the final price; strong QIB subscription usually means the cap price sticks and often aligns with live grey market premium.

No cut‑off option like retail, they pick a price and commit, while small investors can simply choose the cut off price in IPO applications. Allotment? Mostly pro-rata or merchant banker discretion, favoring those who bid high early.

Their stamp of approval boosts retail confidence, smooths listing volatility, and fills the company’s coffers fast.

QIB vs Retail/NII: Spot the Differences

| Feature | QIB | Retail | NII |

|---|---|---|---|

| Bid Size | Unlimited | ≤₹2L | >₹2L |

| Quota | 50% | 35% | 15% |

| Allotment | Pro-rata/Discretionary | Lottery | Pro-rata |

| Withdrawal | Limited | Allowed | Allowed (with rules) |

Retail dreams of lottery luck shaped by factors like IPO application rejected on technical grounds, while QIBs bank on volume and valuation calls.

Why QIB Participation Signals “Green Light”

When HDFC Mutual or BlackRock piles in, it’s a vote of confidence less likely to dump shares day one.

Weak QIB response? Often spells flat or discounted listings. Track live subscription data, QIB oversubscription above 2-3x is your buy cue.

Quick Reality Check for Investors

You can’t become a QIB unless you’re running a fund. Retail folks watch QIB moves via apps or NSE/BSE trackers to gauge hype and compare them with live or upcoming IPOs in the marrket.

Pro tip: Anchor lists in RHPs reveal who’s betting big pre-launch.

QIB in IPO means the institutional muscle, 50% quota, price-setting power, and market-stabilizing heft. They’re a big reason highest listing gain IPO in india while duds struggle. Next time you see heavy QIB bids alongside strong GMP trends and market sentiment, that’s often your signal to lean in.