ICICI Prudential AMC IPO Analysis reveals India’s second-largest AMC by QAAUM at ₹10,147.6 Bn (H1FY26) with 13.2% market share, launching a 00% Offer for Sale (OFS) of 4.9 Cr shares Dec 12-16, 2025.

This pure OFS structure highlights strong profitability (ROE 82.8% FY25) amid ₹67 Tn industry AUM growth at 29% CAGR FY23-25.

ICICI Prudential AMC IPO Dates and Lot Size

ICICI Prudential AMC IPO opens December 12, 2025 (Friday) and closes December 16, 2025 (Tuesday), with allotment by Dec 17, refunds/credit Dec 18, and BSE/NSE listing Dec 19.

Key terms from RHP:

- Issue Size: 4.90 Cr equity shares (100% OFS, no fresh issue)

- Face Value: ₹ 1/share

- Price Band: ₹ 2061 – 2165

- Lot Size: Pending (retail min expected ~₹15,000 at upper band), in line with typical limits on how many lots can be applied in an IPO).

- Reservation: QIB ≤50%, Retail ≥35%, NII ≥15% of net offer.

These levels sit within a premium price band, where understanding the cut‑off price and bid price helps retail investors place smarter bids.

Timeline Table:

| Event | Date |

|---|---|

| Issue Open | Dec 12, 2025 |

| Issue Close | Dec 16, 2025 |

| Basis of Allotment | Dec 17, 2025 |

| Refunds/Credit Shares | Dec 18, 2025 |

| Listing (BSE/NSE) | Dec 19, 2025 |

Retail investors should track the IPO share allotment process and subsequent refund or credit status once these key dates pass.

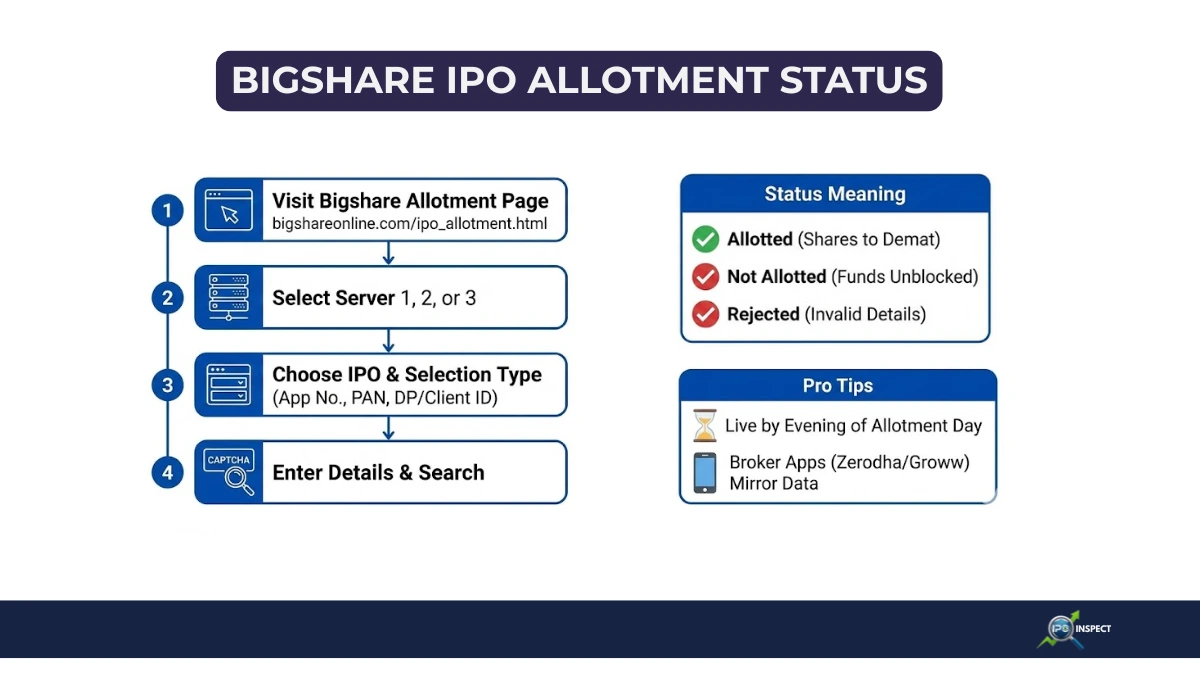

Registrar: Kfin Technologies, where investors typically check their KFintech IPO allotment status.

Lead Managers: Kotak, UBS, ICICI Sec, JM Financial (full list in RHP).

ICICI Prudential AMC IPO GMP Today Latest

ICICI Prudential AMC IPO GMP today stands at ₹345 (Dec 16 update), implying ~100% listing premium over expected cap price, with sub2 sauda rates signaling strong grey market demand.

GMP Trend (Recent):

- Dec 16: ₹345 (upward) estimated listing ₹345, at 15.94% gain shown pre-price band.

- Dec 6: ₹147 (flat, estimated listing ₹147+, 0% gain shown pre-price band.

Trend stable amid high AUM visibility and 82.8% ROE, GMP reflects sector premium but should be treated as a sentiment indicator only, consistent with how IPO GMP reflects market sentiment in other issues

Past grey market premium examples show that strong GMP does not always guarantee high listing gains, so valuation comfort still matters.

Business Overview of ICICI Prudential AMC: Largest Active MF AMC

ICICI Prudential AMC manages India’s largest active MF QAAUM (₹8,635.7 Bn, 13.3% share Sep 2025) plus alternates (PMS/AIF/advisory ₹729 Bn).

Core revenue from investment management fees (94% of total income FY25); serves 15.5 Mn customers via 143 schemes (44 equity-oriented).

Key Products & Reach:

- Mutual Funds: Equity/hybrid leaders (55.8% mix); top schemes: Balanced Advantage (₹658 Bn), Multi-Asset (₹646 Bn)

- Alternates: PMS (₹253 Bn discretionary, largest non-corp), AIF Cat II/III (₹147 Bn), Offshore advisory (₹329 Bn for Eastspring)

- Geography: 272 branches in 23 states/4 UTs; 110K+ distributors + ICICI Bank (7,246 branches)

QAAUM CAGR 32.7% FY23-25 > industry 29%; individual investors 61% of MF AUM.

Industry Overview: MF/AIF/PMS Boom

India’s MF industry QAAUM hit ₹77 Tn (H1FY26, +16.5% YoY); alternates (AIF commitments ₹15.1 Tn, +31-33% to ₹53-56 Tn by FY30). ICICI Pru leads active/equity-oriented (13.6% share) and equity-hybrid (25.8%).

Growth Drivers:

- SIP/STP flows ₹48 Bn (Sep 2025, +23% YoY)

- HNI/UHNI rise fuels PMS/AIF (AMC PMS AUM ₹34 Tn Sep 2025)

- Equity share 54.2%; digital penetration aids retail

Peers: SBI AMC (15.5%), HDFC AMC (11.4%), ICICI Pru outperforms on equity CAGR 40% vs industry 36.2%, making it comparable to names often seen among best‑performing IPOs.

Objects of Issue: 100% Promoter Exit

Pure OFS (₹~14,700 Cr at ₹300 est.):

- No Fresh Issue: Proceeds to selling shareholders (ICICI Bank 51%, Prudential 49% pre-IPO)

- Post-Offer: Promoter holding drops from 100%; supports liquidity, no capex/debt use

Strategic: Unlocks value from ₹46,828 Mn revenue FY25; maintains growth via internal accruals.

Financial Highlights Last 3 Years

Restated standalone (₹ Mn):

| Period | Revenue | EBITDA | EBITDA % | PAT | PAT % | EPS (₹) | ROE % | ROCE %* |

|---|---|---|---|---|---|---|---|---|

| FY23 | 26,892 | 20,726 | ~77% | 15,158 | 56% | 85.9 | 70.0 | NA |

| FY24 | 33,759 | 27,800 | ~82% | 20,497 | 61% | 116.1 | 78.9 | NA |

| FY25 | 46,828 | 36,370 | ~78% | 26,507 | 57% | 150.2 | 82.8 | NA |

| H1FY26** | 27,330 | ~19,328 | ~71% | 16,177 | 59% | 91.6 | 86.8 | NA |

*CFO data limited; **Annualised. Revenue CAGR 32%; PAT 32.2% FY23-25 > peers. Net worth ₹35,169 Mn FY25; debt negligible.

Cash Flow Trends: Stable Operations

Operating Cash Flow: Positive/steady (fee-based model); supports dividends (₹1,140/share FY25 interim). No major mismatches; PAT tracks cash well.

- Investing: Investments in MF/AIFs; capex low (tech/distribution).

- Financing: High dividends to promoters (₹20,124 Mn FY25).

Flag: None; capital-light yields 0.52% revenue yield, 0.36% op margin FY25.

Top Risk Factors from DRHP

Critical risks impacting ICICI Prudential AMC IPO Analysis:

- AUM Volatility: 80%+ revenue from fees tied to markets; equity downturns hit QAAUM.

- Regulatory: SEBI fee caps, TER changes; PMS/AIF norms tightening.

- Competition: 40+ AMCs; flows to passives/SIPs pressure active fees.

- Key Man: CIO/fund managers; redemption risk on performance.

- Cyber/Op Risk: Digital 95% transactions; data breaches.

Contingents manageable vs ₹35 Bn net worth.

Promoters & Management Strength

Promoters: ICICI Bank Ltd (51%), Prudential Corp Holdings (49%); pre-IPO 100%, post-~44% est. No controversies; stable JV since 1998.

Leadership: MD Nimesh Shah (32 yrs exp, CEO of Year 2023); ED/CIO Sankaran Naren (30+ yrs, CIO of Year 2023). Avg KMP tenure 11 yrs; 50 fund managers.

Related Party Transactions Review

Normal arm’s-length with ICICI Group:

- ICICI Bank: ₹389 Mn marketing/common costs, ₹205 Mn trademark, ₹10,263 Mn dividends FY25

- ICICI Securities/Lombard/Life: Minor commissions/insurance (₹57-189 Mn)

No abnormal flags; 94% revenue from ICICI Pru MF (related via sponsor).

Peer Comparison & Valuation vs Listed Peers (FY25 standalone):

| AMC | EPS ₹ | P/E (x) | RoNW % | QAAUM ₹ Bn | PAT ₹ Mn |

|---|---|---|---|---|---|

| ICICI Pru | 150.2 | ~45 est | 82.8 | 8,794 | 26,507 |

| HDFC AMC | 57.6 | 45.2 | 32.4 | 7,740 | ~24,611 |

| Nippon | 20.3 | 41.0 | 31.4 | 5,572 | 12,522 |

| UTI | 57.4 | 19.8 | 16.3 | 3,398 | 6,535 |

| Aditya Birla | 32.3 | 22.5 | 27.0 | 3,817 | 9,247 |

Fairness: Premium P/E (~45x FY25 EPS) justified by #1 active/equity share, 32% revenue CAGR > peers, ROE 82.8% >> 30% avg. At ₹300 GMP, MCAP ~₹53,000 Cr reasonable vs ₹8.8 Tn QAAUM yield.

Red Flags Check: Clean Profile

- Cash vs Profits: Aligned; fee business stable.

- Profit Spike: Organic 32% CAGR FY23-25, no jumps.

- OFS Heavy: 100% OFS (promoter liquidity), but no growth dilution.

- Auditor: S.K. Patodia (clean reports).

- Client Conc: ICICI Pru MF >90% revenue (sponsor-related, stable).

- Litigation: Routine tax/regulatory, no material impact.

No Major Flags for ICICI Prudential AMC IPO Analysis.

Structured Financial Snapshot

Growth Metrics (₹ Bn QAAUM):

| Metric | FY23 | FY24 | FY25 | H1FY26 |

|---|---|---|---|---|

| Total MF | 5.0 | 6.8 | 8.8 | 10.1 |

| Equity-Oriented | 2.5 | 3.7 | 4.9 | 5.7 |

| Individual Investors | 3.2 | 4.6 | 5.7 | 6.6 |

| Alternates | 0.3 | 0.6 | 0.6 | 0.7 |

Conclusion: Subscribe (Long-Term) ICICI Prudential AMC IPO Analysis warrants Subscribe for 3-5 yr horizon, #1 equity/hybrid leadership, 32% CAGR, 83% ROE dwarfs peers despite 100% OFS. GMP ₹3147 eyes for max gains but anchor on ₹10 Tn+ AUM scale amid MF/alternates boom. Skip if avoiding promoter exits. Investors should still read the DRHP key sections, assess their IPO bid strategy, and ensure allocations fit their broader plan for investing.