Employees receiving shares through an IPO, especially via Employee Stock Option Plans (ESOPs) and the employee category in IPO, face specific taxation implications when selling those shares.

Understanding these tax rules helps employees plan their sales tax-efficiently and comply with Indian tax laws.

What Triggers IPO Share Taxation for Employees Selling IPO Shares?

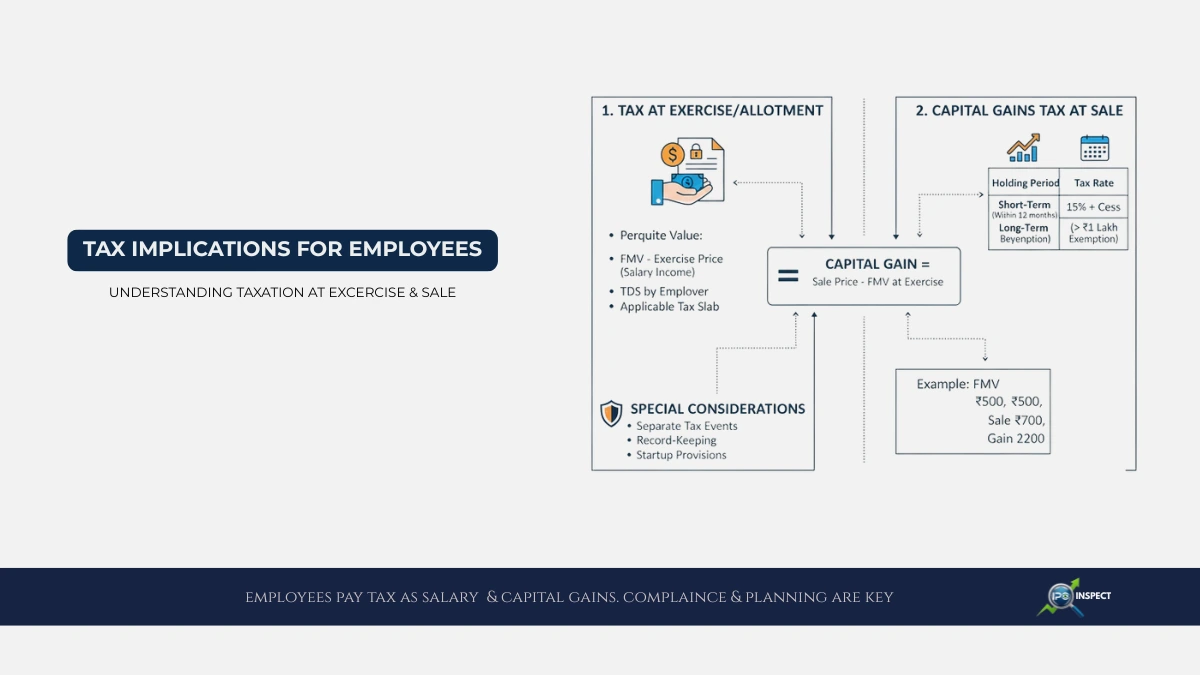

Employees may be allotted shares during an IPO through employee reservation categories, the IPO share allotment process, or ESOP exercises. Taxes on these shares occur at two key points:

- At the time of exercise or allotment as a perquisite (salary income) based on the difference between the fair market value (FMV) and exercise price.

- At the time of sale of shares, capital gains tax applies on the profit made relative to FMV at exercise or allotment.

Taxation on ESOP Shares at Exercise/Allotment

- The perquisite value (FMV less exercise price) treated as part of salary income.

- Tax deducted at source (TDS) by the employer based on applicable income tax slab rates.

Capital Gains Tax When Selling IPO Shares

The capital gains tax depends on how long the shares held after allotment:

- Short-Term Capital Gains (STCG): If shares sold within 12 months of allotment/exercise, gains taxed at 15% plus cess and surcharge.

- Long-Term Capital Gains (LTCG): Holding shares beyond 12 months qualifies for LTCG, taxed at 10% above ₹1.25 lakh exemption limit without indexation benefits.

To better estimate sale price and gains, employees should stay informed about IPO listing price determination, as it significantly affects the eventual capital gain calculation.

Calculating Capital Gains for Employees

Capital Gain = Sale Price – Fair Market Value at Exercise / Allotment

Example: If FMV at exercise = ₹500, sale price = ₹700. Capital gain = ₹200 per share, taxed as STCG or LTCG based on holding period.

Special Considerations

- Employees cannot offset perquisite tax with capital gains tax, the two are separate tax events.

- Proper record-keeping of FMV at exercise and sale price is critical for correct tax filings.

- Additionally, understanding the lock-in period for IPO shares helps employees plan their sale and avoid compliance issues related to restricted trading timelines.

- Tax benefits or exemptions related to ESOPs depend on company classification, e.g., startups have special provisions.

For employees planning future equity sales, tracking upcoming IPOs in India can reveal new opportunities for participation in employee reservation quotas and ESOPs. If shares are not allotted or refunded, checking your IPO refund status is crucial for financial record-keeping and tax compliance.

Conclusion: IPO Share Taxation for employees selling IPO shares or ESOP shares must pay tax as salary income on allotment and capital gains tax on gains at sale. Awareness of these tax rules helps optimize tax liabilities and ensures compliance with Indian Income Tax regulations.